Unlocking Your Home’s Potential: Is a HELOC Right for You?

Your home is more than just where you live—it’s an asset that can work for you. A Home Equity Line of Credit (HELOC) allows you to borrow against your home’s equity, giving you flexible access to funds when you need them. But before we dive into HELOCs, let’s start with the basics.

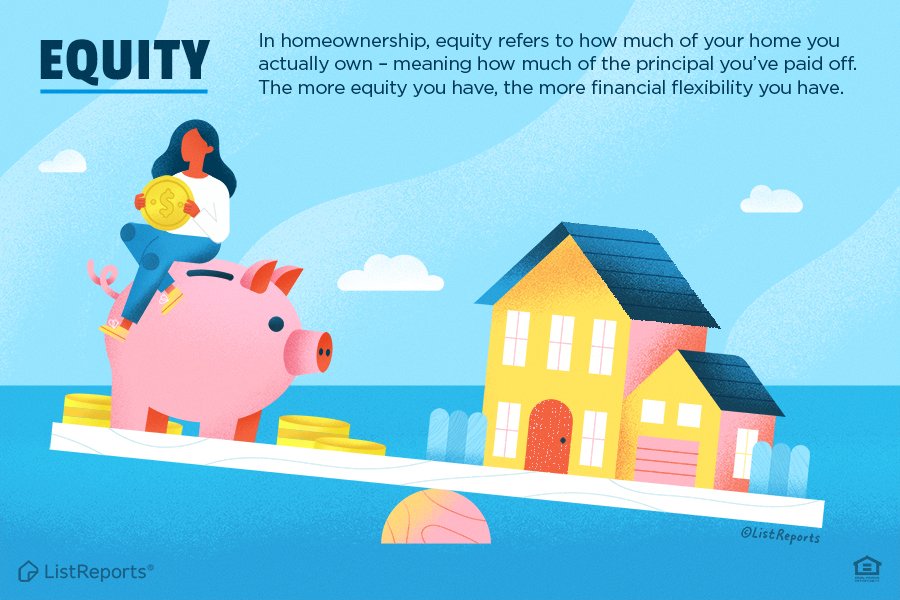

🏡 What Is Home Equity?

Home equity is the portion of your home that you truly own—the difference between your home’s current market value and the amount you still owe on your mortgage.

Example:

Home Value: $400,000

Mortgage Balance: $250,000

Home Equity: $150,000

As you pay down your mortgage and as your home’s value increases, your equity grows. Many homeowners use this equity to secure low-interest financing through options like a HELOC, home equity loan, or cash-out refinance.

🔍 HELOC vs. Home Equity Loan vs. Cash-Out Refinance

There are multiple ways to tap into your home’s equity, and choosing the right one depends on your financial needs. Here’s a quick breakdown:

👉 We’ll review Home Equity Loans and Cash-Out Refinances in an upcoming post, so stay tuned!

✅ How a HELOC Works

A HELOC is a revolving line of credit secured by your home. It functions much like a credit card—you can borrow, repay, and borrow again—up to a set limit. However, it differs from a traditional loan in several ways:

🔹 Draw Period & Repayment Period

Draw Period (5-10 years): During this phase, you can access funds as needed, often using checks or a credit card linked to the HELOC. Minimum payments may only cover interest.

Repayment Period (10-20 years): Once the draw period ends, you must start repaying both principal and interest. Payments may increase significantly at this stage.

🔹 Variable Interest Rates

Most HELOCs have variable interest rates, meaning your payment amount can fluctuate based on market conditions. Some lenders offer an option to convert part of your balance to a fixed rate for more predictable payments.

🔹 Flexible Borrowing

You can typically borrow up to 85% of your home’s equity (home value minus existing mortgage balance).

Funds can be used for home improvements, debt consolidation, emergency expenses, or other financial needs.

🔹 Upfront Costs & Fees

Some lenders charge fees, such as:

✔️ Appraisal fees to determine your home’s value

✔️ Closing costs (title search, mortgage prep, filing fees)

✔️ Annual maintenance fees or transaction fees

🔹 Balloon Payments & Early Termination

If your HELOC requires a balloon payment at the end of the term, you may need to refinance or pay a large lump sum. Some lenders also charge early termination fees if you close the HELOC early.

💡 How a HELOC Helped These Homeowners

🏠 Case #1: Funding Home Renovations Without Draining Savings

Sarah and James wanted to renovate their outdated kitchen and add a home office. Instead of depleting their savings, they used a $50,000 HELOC to fund the project. Since they only withdrew what they needed at different stages of the renovation, they managed cash flow better while enjoying a lower interest rate than a personal loan or credit card.

🏠 Case #2: Smart Debt Consolidation for Lower Payments

Mark and Lisa had high-interest credit card debt totaling $30,000, making monthly payments overwhelming. By tapping into their home equity with a HELOC, they consolidated their debt at a significantly lower interest rate. This not only saved them hundreds per month but also allowed them to pay off their balance faster without the burden of high credit card interest.

🏠 Case #3: Creating a Safety Net for Unexpected Expenses

David and Michelle didn’t need extra funds immediately, but they wanted a financial safety net in case of an emergency. By opening a HELOC, they had access to funds without paying interest unless they used them. When an unexpected medical expense arose, they were able to cover the bill without taking on high-interest credit card debt.

💰 Let’s Find the Best Strategy for You

A HELOC can be a powerful tool—but only if it’s the right fit for your financial goals. Whether you’re looking to renovate, consolidate debt, or prepare for future expenses, I’m here to help you determine the best way to make it happen.

Let’s go over your options together and create a plan that works for you. Reach out today, and let’s start making your home’s equity work for you!